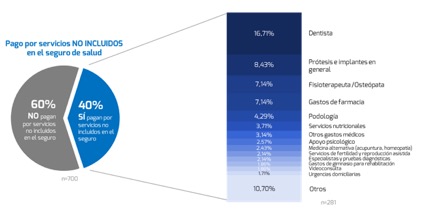

Los asegurados de salud que pagan fuera del seguro gastos de salud representan el 40%. Sus principales gastos son: dentista, prótesis e implantes en general, fisioterapia y osteopatía

Dentro de las especialidades cubiertas por el seguro, las 5 más demandadas son: medicina general, dermatología, traumatología, ginecología / obstetricia y oftalmología

BRAINTRUST, en su IIº Observatorio de la Competencia del Sector Seguros: Ramo Salud al analizar el perfil del tomador del seguro de salud revela que el 40% de ellos pagan por ciertos servicios no incluidos en el seguro, principalmente los relacionados con el dentista (16,71%), prótesis e implantes generales (8,43%) y fisioterapia y osteopatía (7,14%).

Asimismo, el estudio pone de manifiesto que las especialidades del seguro de salud más utilizadas, analizando la frecuencia y el número de veces en la que se utilizan al año, son medicina general, seguido por dermatología, traumatología, obstetricia y ginecología y en quinto lugar oftalmología, mientras que en el extremo opuesto aparecen cardiología, psicología/psiquiatría, neumología y oncología.

Asimismo, el estudio pone de manifiesto que las especialidades del seguro de salud más utilizadas, analizando la frecuencia y el número de veces en la que se utilizan al año, son medicina general, seguido por dermatología, traumatología, obstetricia y ginecología y en quinto lugar oftalmología, mientras que en el extremo opuesto aparecen cardiología, psicología/psiquiatría, neumología y oncología.

Este orden no coincide del todo con el ranking de las veces en las que se usa al año cada una de las especialidades. En la primera posición sigue apareciendo medicina general (2,51 usos al año), pero a partir de la segunda posición el ranking cambia, estando hematología/analítica a continuación (1,47 usos al año) y rehabilitación/fisioterapia en tercer lugar (1,29 usos al año). Las especialidades usadas con menor frecuencia son urología, endocrinología y podología.

Por otra parte, la consultora también ha profundizado en el conocimiento de las expectativas de los usuarios de seguros de salud. En cuanto a servicios no incluidos que les gustaría que incluyera su compañía de salud, la respuesta de los asegurados es muy clara: las más deseadas por los tomadores son: servicios de asistencia para personas mayores, pruebas y perfiles genéticos y chequeos médicos deportivos.

BRAINTRUST también ha preguntado a los usuarios dónde depositarían su confianza en caso de que compañías no especializadas en seguros de salud comercializaran este producto. Según su respuesta, optarían por empresas tecnológicas en un 20,5% y compañías de luz y/o gas en un 18,74%. Menor confianza dan a los operadores de telecomunicaciones, grandes almacenes, compañías e-commerce, empresas de transporte y RR.SS.

A tenor del análisis realizado por BRAINTRUST en su Observatorio de la Competencia del Sector Seguros: Ramo Salud, se desvela una radiografía nítida de las fortalezas y debilidades de la sanidad privada. En cuanto a las primeras, los valores y virtudes de la sanidad privada son muchos, sobresalen su contribución a la sostenibilidad del sistema sanitario, la calidad, flexibilidad, profesionalidad, eficiencia de los profesionales o especialidades; el paciente-cliente es el mejor y mayor crítico y así se constata a la hora de decidirse a contratar un seguro de salud. A su vez, de las respuestas de los propios asegurados, se detectan ciertas debilidades que pueden mejorarse como: ampliar y ofrecer nuevos servicios, impulsar en los seguros privados la cobertura dental, fisioterapia o prótesis para tratar de incrementar el valor de los mismos, de esta manera se eliminarían en buena parte los gastos en servicios no incluidos en el seguro de salud.