-

España es el escenario ideal para el crecimiento de este tipo de entidades

-

Más de 1 de cada 10 españoles ya es cliente de un neobanco

-

El cliente prototipo es menor de 50 años, familiarizado con las nuevas tecnologías y que suele comparar antes de adquirir un producto o servicio

-

Los principales productos que contratan los clientes de un neobanco son de poca vinculación, fundamentalmente cuenta sin nómina y tarjeta de débito

-

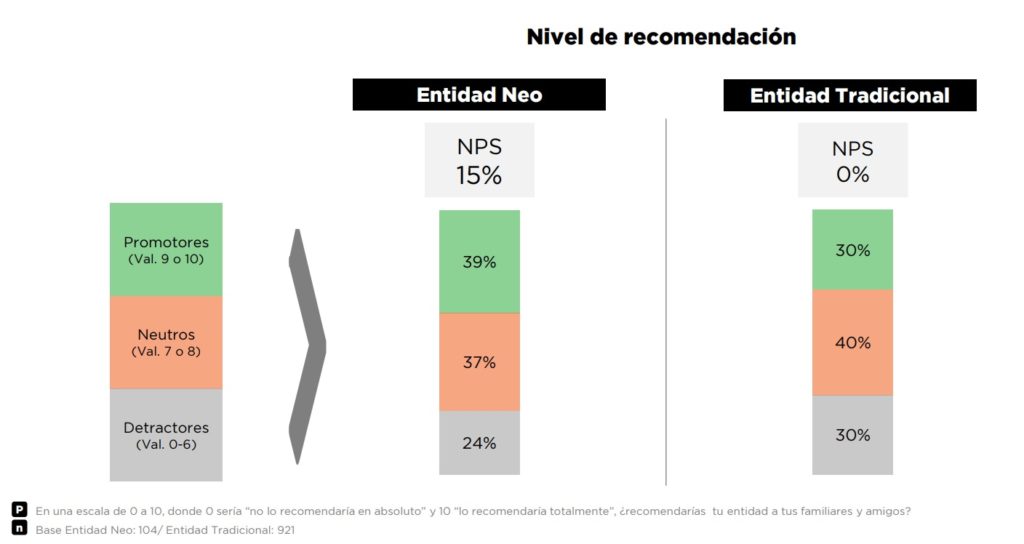

La recomendación de los clientes de neobancos es superior a la de las entidades tradicionales

Según el primer Observatorio de Banca Digital realizado por BRAINTRUST, España es un escenario ideal para el crecimiento de neobancos, con un 98,3% de la población mayor de 15 años bancarizada.

En 2021 el 95,9% de los hogares disponía de banda ancha y un 91,8% de las personas usó internet regularmente. Entre las actividades más realizadas, en séptima posición, se encuentra el uso de la banca por internet con un 65,2% y el total de cuentas bancarias activas en bancos digitales rozaba los 9 millones al final de 2020.

Este terreno de juego invita a los neobancos a potenciar y mejorar su oferta en nuestro país y cada vez más entidades se posicionan en España para captar clientes en un segmento en el que, a pesar del rápido crecimiento, la oportunidad es todavía muy grande.

Uno de cada diez españoles es cliente de un neobanco

Cabe recordar que los neobancos son entidades financieras exclusivamente digitales, mientras que la banca digital es una extensión de los bancos tradicionales que han adaptado sus servicios al entorno en línea. Los neobancos suelen ser empresas independientes que operan sin sucursales físicas, mientras que la banca digital es ofrecida por bancos establecidos que tienen tanto presencia física como canales en línea.

Los clientes de Neobancos suponen ya un 11,3% del total de la población bancarizada o, dicho de otro modo, más de 1 de cada 10 españoles es cliente de un neobanco. El 75% de estos clientes son clientes mixtos, es decir, son clientes de un neobanco y además los son de otra entidad de las denominadas tradicionales. El otro 25% solo dispone de cuenta en un neobanco.

Respecto a las zonas, Centro y Levante destacan por ser las que cuentan con una mayor penetración de este tipo de entidades, mientras que en Norte y Cataluña muestran algo más de resistencia a la hora de convertirse en cliente de este tipo de bancos 100% digitales.

Perfil del cliente de un neobanco: menor de 50 años, tecnológico, con estudio superiores e ingresos medios-altos.

Según el observatorio de banca digital elaborado por BRAINTRUST, el 80% de los clientes de neobancos tienen menos de 50 años. A partir de esa edad, la penetración de este tipo de entidades baja entre la población.

El cliente de neobanco, en comparación con el de otro tipo de entidades, tiene clara preferencia por las gestiones online, se considera muy tecnológico y toma en cuenta comentarios de otros usuarios antes de tomar decisiones de compra. Al estar muy familiarizados con las tecnologías, declaran realizar compras online, pagar con el móvil, usar Bizum o compartir contenido en redes sociales con una frecuencia superior a los clientes de entidades bancarias tradicionales.

En esa línea, se consideran personas reflexivas a la hora de comprar o contratar un producto o servicio, comparando y dedicando tiempo a elegir lo más adecuado a sus intereses.

Para Jose Manuel Brell, Director del Observatorio, y Responsable del Área de Banca y Servicios financieros en BRAINTRUST: “Dado el prototipo de cliente que en la actualidad presenta este tipo de entidades, los neobancos se enfrentan a un desafío doble: Por un lado, a corto plazo, ser capaces de hacer llegar su oferta a nuevos nichos de mercado entre los que actualmente están teniendo poco éxito (fundamentalmente personas de edad media con cierto hábito tecnológico), consiguiendo que dejen de percibir a los neobancos como entidades solo para “modernos”, “tecnológicos” o jóvenes. Por otro, la tremenda oportunidad que representa a medio-largo plazo un cliente que cada vez cumplirá más con ese perfil tecnológico sea cual sea su edad, en un contexto en el que; eso sí, la competencia entre entidades digitales (sean “puras o no) será cada vez mayor.”

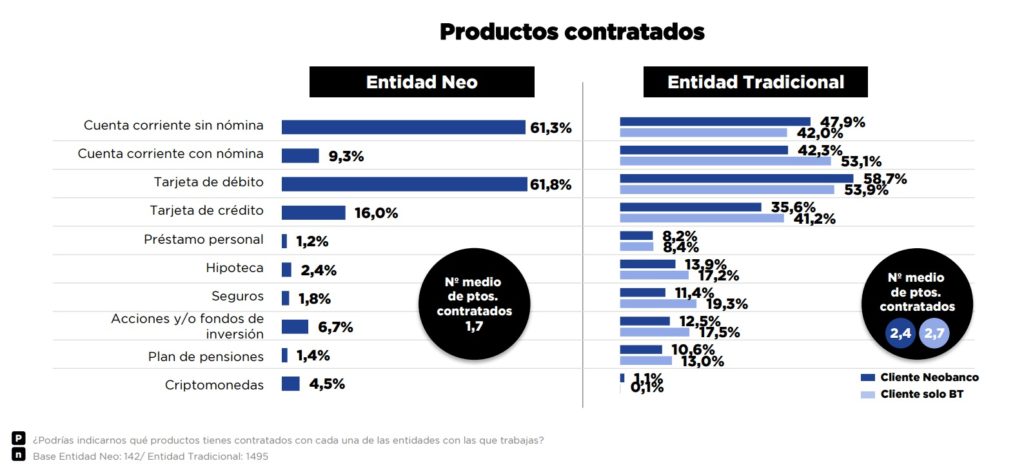

El cliente de neobancos empieza poco a poco: productos básicos y de poca vinculación

Otro hecho destacado que pone de manifiesto el Observatorio de Banca Digital elaborado por BRAINTRUST es la contratación de productos básicos (cuenta sin nómina y tarjeta de débito, fundamentalmente, y siempre sin comisiones) como primera toma de contacto de los clientes con los neobancos.

Según el Observatorio, la media de productos contratados por los clientes de neobancos es 1,7 frente a los 2,7 de los clientes de entidades tradicionales. Si bien es cierto que la gama de productos ofrecidos por los neobancos es mucho más reducida y menos compleja de la que otras entidades, destaca que solo el 9,3% de los clientes de neobancos cuentan con su nómina en esa entidad y que solo el 16% solicita una tarjeta de crédito.

Los nuevos entrantes llevan tiempo trabajando en revertir esta tendencia, ampliando su porfolio de productos y ofreciendo cada vez mejores ofertas y promociones de bienvenida a los clientes que apuesten por ellos con cierta vinculación (trayendo la nómina o un manteniendo un saldo medio mínimo generalmente), a la vez que algunas entidades van adquiriendo notoriedad para conseguir superar esa primera barrera del posible desconocimiento o miedo a ser el primero en probar algo nuevo por parte del cliente.

Analizando el patrón de uso de otros productos financieros, se observa que los clientes de neobancos son los que más productos tienen en otras plataformas de servicios financieros más allá de los bancos, más en concreto en plataformas de criptomonedas y de transferencia de dinero y divisas. En el lado opuesto, hipotecas y seguros de hogar y vida son los que más se contratan con la entidad bancaria, por la sensación de seguridad y por la ausencia de este tipo de productos en muchos de las nuevas entidades 100% digitales.

Destaca el porcentaje de clientes de neobancos que no cuentan con ningún tipo de seguro, posiblemente relacionado con el perfil joven de clientes de este tipo de entidad.

La recomendación de los clientes de neobancos es superior a la de las entidades tradicionales

Las entidades neo cuentan con un nivel de recomendación mayor que las tradicionales. En el conjunto de los neobancos, el 39% de sus clientes valoran la recomendación de su entidad con un 9 o 10 mientras que el 24% lo hace por debajo de 6, lo que sugiere un indicador NPS (Net Promoter Score) de +15.

En el caso de las entidades tradicionales, los promotores y detractores se sitúan al mismo nivel, dando lugar a un NPS de 0.

Para los clientes más digitales son sobre todo las comisiones, pero también la facilidad y comodidad, y la posibilidad de hacer operaciones desde el extranjero lo que más les lleva a recomendar a sus entidades a familiares y amigos. Los clientes más tradicionales del sector bancario, recomiendan por la calidad del servicio y profesionalidad y la confianza y seguridad en la entidad.

Poder contar con atención personal en el banco es especialmente importante para aquellos clientes exclusivamente de bancos tradicionales, sobre todo en términos de contratar o abrir una cuenta, contratar una hipoteca o recibir cualquier tipo de asesoramiento. Los clientes de neobancos consideran suficiente la atención a través del teléfono, WhatsApp u online.

Sin embargo, en todo tipo de clientes, la atención presencial es muy bien valorada para contratar préstamos, hipotecas o productos de inversión.

Foto de Rodion Kutsaiev en Unsplash